On May 15, 2026, the Bureau of Indian Standards quietly published a notification that will shape India’s clean fuel future for the next decade. IS 19850:2026 formally established technical specifications for E22, E25, E27, and E30 fuel blends – petrol blended with up to 30% ethanol – for use in positive-ignition engine vehicles.

Industry bodies welcomed it. The All India Distillers’ Association called it a “critical step.” Ethanol producers, sitting on surplus capacity, saw a long-awaited demand signal. The political logic was clean: less imported crude, more rural income, lower transport emissions.

But behind the policy momentum, two quieter questions are gathering force in independent research, government data, and even within NITI Aayog’s own warnings:

- Where will the feedstock for E30 come from?

- How much food and how much water will India have to give up to get there?

The answers matter. Because if India tries to reach E30 the way it reached E20 – by leaning harder on sugarcane, maize, and rice – the country could end up trading one form of import dependence (oil) for two others India can far less afford to lose: food security and groundwater.

This is the structural case for why E30 cannot be built on first-generation ethanol alone. And why second-generation (2G) ethanol – made from agricultural residues like rice straw – is no longer an alternative pathway. It is the only sustainable one.

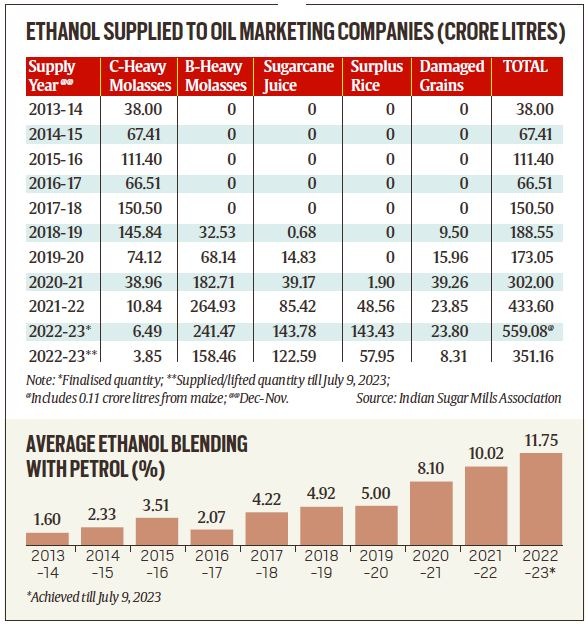

Where India Stands: From E20 Achieved to E30 Notified

India’s ethanol blending journey has moved at a remarkable pace:

- ~1.5% blending in 2014 → 14.6% in 2023–24 → 20% by April 2026

- The E20 target was hit nearly five years ahead of the original 2030 deadline.

- Installed ethanol production capacity has grown from 420 crore litres in 2013–14 to roughly 2,000 crore litres by late 2025, with another 400 crore litres expected by FY27.

- Over ₹1.25 lakh crore has flowed to farmers through ethanol procurement, and over ₹1.44 lakh crore has been saved in foreign exchange through reduced crude imports.

Against this track record, the BIS notification for E22–E30 isn’t a leap. It’s the logical next step. The Petroleum Ministry has already commissioned ARAI to study E25’s impact on existing vehicles. A government committee is preparing the roadmap beyond E20 – with E27 and E30 squarely in view.But the question that the notification does not answer is the one that matters most: what will fuel the fuel?

The Food Question: 1G Ethanol Is Now Eating Into the Public Distribution System

To understand how serious the food-vs-fuel trade-off has become, look at what changed in March 2026.

The Centre announced that the share of broken rice in grains distributed under the Public Distribution System (PDS) would be cut from 25% to 10%. The 15-percentage-point gap – roughly 90 lakh tonnes (9 million metric tonnes) of broken rice annually – would be redirected to ethanol distilleries.

Put plainly: rice that was being eaten by 80 crore PDS beneficiaries will now be converted into automotive fuel.

This is not an isolated policy choice. It is part of a clear trajectory:

| Year | FCI broken rice diverted to ethanol | Policy lever |

| Ethanol Supply Year 2024–25 | ~52 lakh tonnes (5.2 million MT) | FCI surplus rice auctions to distilleries |

| Ethanol Supply Year 2025–26 (target) | ~90 lakh tonnes (9 million MT) | Broken rice in PDS reduced from 25% to 10% – surplus 15% redirected to ethanol |

| E25 demand scenario (2027–28) | Substantially higher if 1G-dependent | Likely additional rice / maize / sugarcane diversion |

| E30 demand scenario (BIS-notified, post-rollout) | Structurally unworkable on 1G alone | Requires 2G ethanol at scale |

Defenders of the policy argue, with some justification, that India is sitting on surplus rice. FCI’s rice buffer norm is around 13.5 million tonnes; actual stocks have ballooned past 50 million tonnes – roughly four times the buffer requirement. From this angle, ethanol is absorbing waste, not taking food off the table.

But that argument has cracks that widen as blending scales:

- Surplus is a feature of bad logistics, not abundance. As the Comptroller and Auditor General has noted repeatedly, FCI surpluses reflect procurement and redistribution inefficiencies – not surplus food in the system. The same grain could fortify school meals, anganwadi programmes, urban nutrition schemes, or function as a strategic buffer against climate-driven supply shocks.

- “Broken” rice is not unfit for human consumption. It is whole rice with broken kernels – still nutritionally identical. Categorising it as industrial feedstock is a policy choice, not a biological reality.

- The mechanism is structural, not transitional. Cutting PDS broken rice allocation from 25% to 10% means the diversion is now baked into the supply chain. Reversing it would require re-engineering procurement norms across five major rice-producing states.

- Demand will keep climbing. E20 absorbs roughly 1,050 crore litres of ethanol per year. E25 will push that toward 1,300–1,400 crore litres. E30, if rolled out, will need substantially more – and at higher blends like E85 or E100 (under flex-fuel scenarios), industry estimates point to 15–25 billion litres of additional dependable capacity being required.

Each step up the blending curve, if delivered through 1G ethanol, increases the volume of food crops being diverted from kitchens to fuel tanks. At E30, that volume becomes structurally large enough that it cannot be defended as “surplus absorption” anymore. It is a deliberate reallocation of the food system into the fuel system.

The Water Question: Trading Oil Dependence for Water Depletion

If the food story is uncomfortable, the water story is alarming.

Earlier in 2026, NITI Aayog’s Composite Water Management Index reiterated a warning that should be impossible to ignore: groundwater in 21 major Indian cities – including Delhi, Bengaluru, Chennai, and Hyderabad – is on track toward critical depletion by 2030.

India’s per capita water availability has already fallen to roughly 1,486 cubic metres (2021) – placing it firmly in the “water-stressed” category. Projections suggest it will drop to around 1,140 cubic metres by 2050. Agriculture, meanwhile, consumes nearly 80% of the country’s freshwater.

Against that backdrop, here is what each litre of 1G ethanol actually costs India in water:

| Feedstock pathway | Generation | Water per litre of ethanol | Source of water |

| Rice (paddy) | 1G | ~10,790 litres | Heavy irrigation; groundwater-fed in Punjab, Haryana, UP |

| Maize | 1G | ~4,670 litres | Mix of rain-fed and irrigated; lower than rice |

| Sugarcane (molasses) | 1G | ~3,630 litres (some estimates ~2,860 L per NITI Aayog 2021) | High irrigation; concentrated in water-stressed Maharashtra, Karnataka, UP |

| Rice straw / agricultural residue (2G) | 2G | Negligible (process water only – feedstock is already waste) | No new agricultural water demand |

These numbers – the rice figure cited by the Food Secretary himself, the sugarcane figure from NITI Aayog’s 2021 ethanol roadmap, and the maize figure from government data – describe a fuel pathway whose hidden price is paid not at the pump but at the borewell.

A litre of ethanol made from rice can consume nearly 11,000 litres of water across cultivation and processing. India is not just converting grain into fuel – it is converting irrigation water and groundwater into automobile exhaust.

The Geography Makes It Worse

It is not just the volume of water that matters. It is where the water is being drawn from.

- Maharashtra – facing recurring droughts in Vidarbha and Marathwada – hosts ethanol plants with a combined capacity of roughly 396 crore litres, much of it sugarcane-based.

- Uttar Pradesh and Karnataka ethanol plants draw from groundwater reserves already classified as critically depleted.

- Punjab and Haryana rice growers have been blamed for decades for depleting groundwater. Now the same rice is being industrially converted into fuel – yet the industry is not held to the same scrutiny.

Even NITI Aayog’s own 2021 ethanol blending roadmap explicitly acknowledged the heavy water burden of 1G feedstocks and recommended a shift toward more water-efficient alternatives and advanced second-generation biofuels. Five years later, the warning has only become more urgent.

The Wastewater No One Talks About

There is a third dimension to the water story that rarely makes the headlines: vinasse. Ethanol distilleries produce large volumes of vinasse – a high-organic-load wastewater that, if not treated to strict standards, contaminates surface water and groundwater. Scaling up 1G ethanol means scaling up vinasse generation in the same water-stressed regions where the feedstock is being grown.In short: 1G ethanol uses water to grow the crop, uses water to process it, and risks polluting water as it disposes of the byproduct. Three water hits per litre. And every one of those hits is concentrated in states that are already running short.

Why 2G Ethanol Solves Both Problems – At Once

This is the moment where second-generation ethanol stops being an academic concept and becomes the most important fuel pathway in India’s energy transition.

2G ethanol is produced from lignocellulosic biomass – agricultural residues that are either burned in fields, used for low-value applications, or left to rot. The most abundant feedstock is rice straw (paddy straw), of which India generates roughly 160–180 million tonnes every year – a significant share of which is currently set on fire in Punjab and Haryana, contributing to North India’s winter air pollution crisis.

Compare that to 1G ethanol on the two dimensions that define this debate:

On Food

- 1G ethanol takes food crops or food-grade grain (sugarcane, maize, rice) and converts them into fuel.

- 2G ethanol uses the residue left after the food has already been harvested. The grain still goes to the kitchen. The stubble – which was going to be burned anyway – goes to the fuel tank.

On Water

- 1G ethanol carries the full water footprint of the crop – 3,000 to 11,000 litres per litre of ethanol, depending on the feedstock.

- 2G ethanol uses only process water (a few litres per litre of ethanol). The crop was grown for food; the residue is a free byproduct. No new agricultural water demand is created.

Put together, 2G ethanol is the only pathway that allows India to scale toward E25, E27, and E30 without enlarging the food-fuel conflict and without deepening the groundwater crisis.

It also delivers four additional benefits that 1G cannot:

- It eliminates a public-health hazard. Every tonne of rice straw converted into ethanol is a tonne not burned in an open field.

- It creates a circular bio-economy. The same biomass yields ethanol, plus high-purity precipitated silica, plus gypsum – multiple revenue streams from a single residue stream.

- It is feedstock-resilient. Agricultural residues are generated regardless of whether sugar prices spike or grain markets tighten.

- It produces deeper lifecycle carbon savings, because the alternative for the feedstock was either combustion (releasing CO₂ anyway) or decay (releasing methane).

Policy Has to Catch Up With Physics

India’s biofuel policy framework has been built on the assumption that 1G ethanol can carry the country to higher blending mandates. The data – on food diversion, on water footprint, on regional groundwater stress – is increasingly making that assumption untenable.

Three policy shifts are now overdue:

- A defined feedstock cap on 1G ethanol. The total volume of food-grade rice, sugarcane juice, and maize that can be diverted to ethanol annually should be capped – preferably at or near current levels – with all incremental demand from E25/E27/E30 met from 2G pathways.

- Differential pricing that reflects the true cost of 1G ethanol. If 2G ethanol is more capital-intensive but uses no incremental water and no food, the pricing structure should compensate for that – not penalise it. The current pricing regime undervalues the externalities saved by 2G.

- Aggressive scaling of 2G capacity. BPCL’s commercial 2G plant at Bargarh, Odisha (commissioned March 2026, processing 100 KLPD from rice straw) is a proof point. PM JI-VAN Yojana provides the scheme. What is missing is execution velocity – and that requires biomass aggregation policy, faster land acquisition, and risk-sharing on first-of-a-kind 2G plants.

Where Khaitan Bio Energy Fits In

The case for 2G ethanol becomes meaningful only when the technology to produce it works economically and at scale. That has been the longstanding gap in India’s biofuel ecosystem – and it is the gap [Khaitan Bio Energy](https://khaitanbioenergy.com/) was built to close.

The company’s patented 2G ethanol technology, developed by Mr Rohit Khaitan and validated through a BIRAC-supported pilot under the “Cellulosic Ethanol Pilot Plant for Rice Straw Management” project, establishes a commercially viable cellulose-to-sugars-to-ethanol pathway.

Three credentials matter in the context of the E30 conversation:

- The technology is certified at Technology Readiness Level 8 (TRL-8) by the Department of Biotechnology, Government of India – meaning it is ready for commercial deployment, not still in lab stages.

- It is the rare 2G platform that fully utilises every component of lignocellulosic biomass – delivering not only ethanol, but also high-purity precipitated silica and gypsum as co-products. This breakthrough in lignin valorisation is what transforms 2G unit economics from marginal to competitive.

For an India trying to scale to E30 without burning more food and draining more groundwater, this kind of platform is not optional. It is the bridge between what policy is targeting and what the country can actually sustain.

The Road Ahead

The E30 standards notified by BIS in May 2026 are an enormous opportunity. They signal that India is serious about energy sovereignty, serious about supporting rural incomes, and serious about decarbonising transport. None of that is in dispute.

What is in dispute is the path. If India tries to reach E30 by pouring more rice, sugarcane, and maize into distilleries, the country will trade its imported-oil problem for two problems it is far less equipped to solve: a food security problem and a water security problem.

If, instead, India scales to E30 by building out 2G ethanol capacity – turning the rice straw that is currently burning into fuel, and leaving the food crops where they belong – the same blending mandate becomes one of the most powerful sustainability levers any major economy has ever pulled

The fuel is the same number on the petrol pump. The path determines whether E30 is a triumph or a trade-off.

Frequently Asked Questions

Q1. What is E30 fuel and is it available now in India?

E30 is petrol blended with 30% ethanol. On May 15, 2026, the Bureau of Indian Standards notified IS 19850:2026, formally establishing technical specifications for E22, E25, E27, and E30 fuel blends. The notification does not immediately mandate the nationwide sale of E30 – it creates the regulatory and technical foundation for a phased rollout. ARAI is currently studying engine compatibility for higher blends starting with E25.

Q2. How does 1G ethanol affect food security in India?

First-generation (1G) ethanol is produced from food crops – primarily sugarcane, maize, and rice. In March 2026, the government reduced the share of broken rice in PDS allocations from 25% to 10%, redirecting roughly 90 lakh tonnes (9 million tonnes) of rice annually from the public food distribution system to ethanol distilleries. As blending mandates rise from E20 toward E25 and E30, the volume of food crops being diverted to fuel will grow substantially.

Q3. How much water does it actually take to produce one litre of ethanol?

It depends entirely on the feedstock. Using Food Secretary and NITI Aayog data: rice-based ethanol uses approximately 10,790 litres of water per litre of ethanol (cultivation + processing); maize uses around 4,670 litres; sugarcane uses approximately 3,630 litres (some NITI Aayog estimates put it at 2,860 litres). In contrast, 2G ethanol made from rice straw uses only a few litres of process water per litre of ethanol – because the feedstock is agricultural residue, not a separately grown crop.

Q4. Isn’t India producing surplus rice that would otherwise go to waste?

FCI stocks have indeed exceeded buffer norms – but as the CAG and standing committee reports have pointed out, this reflects procurement and storage inefficiencies, not genuine food surplus. The same grain could be redirected to fortified school meals, anganwadi programmes, disaster relief, and urban nutrition schemes, or held as a strategic buffer against climate-driven supply shocks. “Broken” rice is also nutritionally identical to whole rice – categorising it as industrial feedstock is a policy choice.

Q5. How does 2G ethanol solve the food and water problem simultaneously?

2G ethanol uses lignocellulosic biomass – primarily agricultural residues like rice straw, wheat straw, and bagasse – that are left over after the food crop has already been harvested. The grain still goes to the kitchen; the stubble (which would otherwise have been burned or left to decay) goes to the fuel tank. Because the crop wasn’t grown for ethanol, no incremental water is consumed, and no food is diverted. It is the only pathway that genuinely decouples ethanol scale-up from food and water pressure.

Q6. What is NITI Aayog warning about India’s groundwater?

NITI Aayog’s Composite Water Management Index has warned that 21 major Indian cities – including Delhi, Bengaluru, Chennai, and Hyderabad – face critical groundwater depletion by 2030. India’s per capita water availability has fallen to ~1,486 cubic metres (2021) and is projected to drop to ~1,140 cubic metres by 2050. Agriculture already uses ~80% of India’s freshwater. Scaling 1G ethanol in this context adds an industrial claimant to the same shrinking water base

Q7. How is Khaitan Bio Energy positioned for India’s E30 transition?

Khaitan Bio Energy holds patents for a 2G ethanol production technology certified at TRL-8 by the Department of Biotechnology and selected for commercial biorefinery development under the PM JI-VAN Yojana. The technology converts rice straw and other lignocellulosic biomass into ethanol – without competing with food crops or drawing additional agricultural water – and uniquely valorises lignin to produce high-purity silica and gypsum as co-products. For an E25-to-E30 future, this is exactly the kind of platform India’s energy transition will rely on.