In the first week of June 2026, India’s flex-fuel story moved out of the policy pages and into the showroom.

On June 3, Hero MotoCorp -India’s largest two-wheeler manufacturer -launched two flex-fuel motorcycles in its highest-volume segment: the Splendor+ Flex Fuel and the HF Deluxe Flex Fuel. Both can run on ethanol blends from E20 all the way to E85, making them India’s first flex-fuel motorcycles in the 100cc commuter category.

A day later, on June 4, Maruti Suzuki unveiled the Wagon R Flex Fuel (“Bioflex”) in New Delhi -India’s first flex-fuel passenger car, engineered to run on petrol-ethanol blends all the way up to E100. The launch was attended by Union Petroleum Minister Hardeep Singh Puri, and timed deliberately for the day before E85 fuel itself went on retail sale at 48 IndianOil outlets.

Hero and Maruti are not premium niche players. They are the two manufacturers whose combined volumes account for a substantial share of all new vehicles sold in India every year. The Wagon R, the Splendor+, and the HF Deluxe are the cars and bikes that families, office-goers, delivery riders, and small business owners actually buy. Putting flex-fuel technology in these specific models -not in concept cars, not in luxury imports -is the clearest signal yet that India’s flex-fuel transition is moving from intent to volume.

Which makes the next question unavoidable. If flex-fuel demand scales the way Hero and Maruti are now positioning it to scale, where will the ethanol come from?

Because the supply-side answer cannot be 1G ethanol alone. Not at this scale. Not for this long.

What Was Actually Launched, and Why It Matters

| OEM | Model(s) | Launch date / segment | Ethanol blend capability |

| Hero MotoCorp | Splendor+ Flex Fuel, HF Deluxe Flex Fuel | June 3, 2026 -India’s first 100cc-segment FFV motorcycles | E20 to E85 |

| Maruti Suzuki | Wagon R Flex Fuel (“Bioflex”) | June 4, 2026 -India’s first flex-fuel passenger car | Up to E100 |

| Tata Motors PV | Maiden FFV (model TBD) | Targeted: early 2027 | Flex-fuel platform |

| Toyota Kirloskar | Innova Hycross Flex-Fuel Strong Hybrid | Active pilot (homologation in progress) | Flex-fuel + hybrid |

| Suzuki Motorcycle | Gixxer SF 250 (E85) | Already on sale (premium segment) | E85 |

| Honda Motorcycle | CB 300F (E85) | Already on sale (premium segment) | E85 |

Read across this table, and the structural picture becomes clear: flex-fuel is no longer a single-launch story or a premium-segment experiment. It is a mass-market, multi-OEM, multi-segment shift happening within a defined window.

Three details from the launches are worth pulling out

Hero’s choice of models is deliberate

The Splendor+ and HF Deluxe are among the highest-selling motorcycles in India by volume. Hero CEO Harshavardhan Chitale told Business Today that the company sees flex-fuel as part of a broader “energy resilience” thesis -explicitly framing FFVs as a way to reduce India’s dependence on imported battery cells (almost entirely sourced from China) in the same conversation as imported crude oil. With EV penetration in two-wheelers stagnating at roughly 7% over the past two years, FFVs are emerging as a parallel -not competing -pathway to clean mobility.

Maruti went straight to E100 capability

The Wagon R Bioflex is not just E85-capable. It is engineered for up to 100% ethanol -meaning that as the retail network matures and dedicated pumps offering pure ethanol (E100, similar to Brazil’s hydrous-ethanol model) come online, the vehicle is already compatible. Maruti has effectively future-proofed its launch against the entire E20-to-E100 range.

The pricing tells us where adoption will lead first

The Wagon R Flex is priced at ₹7.24 lakh ex-showroom -roughly ₹85,000 more than a comparable petrol Wagon R, a premium of about 12%. Hero’s flex-fuel motorcycles, by contrast, are priced only ~4% above their petrol equivalents. That gap matters: two-wheelers will reach mass adoption first, because the affordability calculation flips earlier for daily commuters, delivery riders, and rural users whose two-wheeler is a working asset, not a discretionary purchase.

Maruti’s “Three Pillars” Framework -and What Each Pillar Now Demands

In a conversation with analysts following the launch, Rahul Bharti, Senior Executive Officer at Maruti Suzuki, framed the FFV opportunity around three pillars that must align for flex-fuel to scale:

| Pillar | Status as of June 2026 | What still needs to happen |

| 1. The vehicle | Hero (two-wheelers) and Maruti (passenger car) launched in the same week. Tata, Toyota and others in the pipeline. | Affordability gap: Wagon R Flex priced ~₹85,000 over conventional petrol Wagon R (~12% premium). Two-wheeler premium is only ~4%. |

| 2. The fuel network | E85 retail launched June 5, 2026 at 48 outlets. Plan: 500 by Dec 2026, 5,000 by Dec 2027. | Rollout needs to keep pace with vehicle launches; otherwise FFV owners face fuel availability gaps outside metros. |

| 3. The price differential | E85 launched at ~₹20/litre below petrol -strong consumer signal. | Differential must remain durable to offset ethanol’s lower energy density (mileage hit). Requires stable ethanol supply at competitive cost. |

Bharti’s own assessment is candid: in the near term, FFV volumes will remain limited because the ethanol-petrol price parity is still finding its footing and the retail network is still small. He estimates meaningful FFV volumes are five to ten years out.

But that is the consumer-side timeline. The supply-side preparation has to begin now, because building 2G ethanol production capacity takes years from financial close to commercial operation. By the time the third pillar -durable ethanol pricing -is needed at scale, the feedstock infrastructure has to already be in place.

The Headwinds -Honestly Assessed

The mainstream coverage of the Hero–Maruti launches has flagged four genuine challenges. Each is real. Each is also addressable -but only if the supply side moves with the demand side.

1. Mileage trade-off

Ethanol has roughly two-thirds the energy density of petrol. A litre of E85 doesn’t take you as far as a litre of petrol. UCAL Ltd’s joint MD Adithya Jayakar has indicated consumers could see 25–35% lower per-kilometre fuel costs on E85 -but only if ethanol pricing stays meaningfully below petrol on an energy-equivalent basis. JATO Dynamics’ Ravi Bhatia has warned that on E100, the energy-density gap is large enough that running cost savings

could be partially offset, depending on prices. Durable ethanol pricing is the difference between flex-fuel being a winning consumer proposition and a punitive one.

2. Refuelling infrastructure

E85 and E100 are not drop-in replacements for petrol. They need corrosion-resistant storage tanks, dedicated dispensing pipelines, and moisture-controlled handling because ethanol is hygroscopic. Forty-eight stations on Day One is symbolic; 5,000 stations by end-2027 is the milestone that actually matters. Hero CEO Chitale was direct: “as soon as fuel starts becoming available, the industry can introduce flex-fuel vehicles pretty much in the same month.” OEMs are not the bottleneck. The pump is.

3. Vehicle affordability

A ₹85,000 premium on a Wagon R is non-trivial in the segment Maruti sells most of its volume into. Industry executives have suggested targeted GST reductions on FFVs (currently 18% for petrol two-wheelers under 350cc) and meaningful state-level incentives. The draft CAFE III norms have reduced FFV super-credits from 1.5 to 1.1 -a policy headwind that automakers are flagging. The vehicle premium has to come down for mass adoption to follow.

4. Long-term ethanol supply credibility

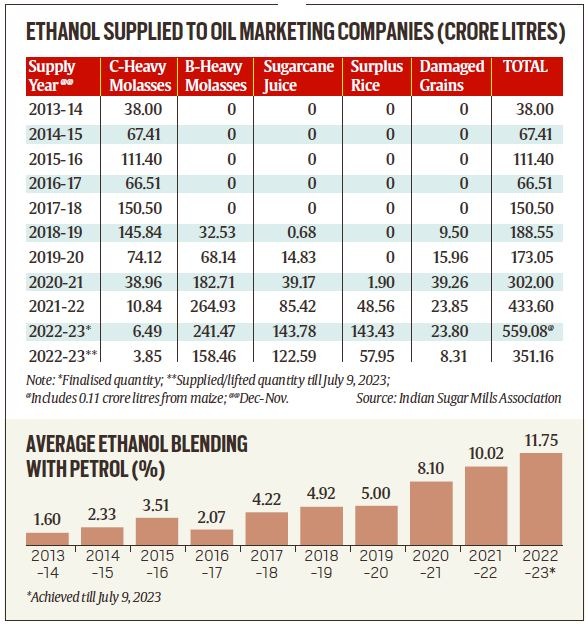

This is the headwind that does not get enough airtime. If India’s FFV fleet scales -Hero, Maruti, Tata, Toyota and others -through the late 2020s and into the 2030s, the country has to commit to a multi-decade ethanol supply trajectory that consumers, OEMs, and fuel retailers can underwrite. That commitment cannot rest on sugarcane, maize, and rice alone. The water, land, and food-security ceilings on 1G ethanol are already visible -and they tighten further with every additional megalitre of demand.

Why the OEM Launches Make 2G Ethanol Urgent, Not Optional

There is a direct line between the cars and bikes launched in the first week of June 2026 and the kind of ethanol India needs to produce over the next decade.

Consider the demand math:

- Each Wagon R Flex running on E85 consumes roughly 85% of its fuel volume as ethanol -versus 20% on an E20 petrol car.

- Each Splendor+ Flex Fuel rider on E85 is, on a volume basis, an order of magnitude larger ethanol consumer than the same rider on E10 or E20 fuel.

- InCred Research’s recent projection (covered in our companion piece on the E85 launch) estimates that flex-fuel adoption could lift India’s annual ethanol demand from approximately 13 billion litres in FY 2026 to 29.63 billion litres by FY 2040 -a 21% uplift above the E20-only base case.

That demand cannot be met sustainably with 1G ethanol. The structural ceilings are well-documented:

- Sugarcane is highly water-intensive (~3,630 litres of water per litre of ethanol) and concentrated in already water-stressed Maharashtra, UP, and Karnataka.

- Maize is already a major poultry feed input -additional diversion raises livestock and food prices.

- Rice diversion to ethanol has already cut the PDS broken-rice allocation from 25% to 10%, moving ~90 lakh tonnes annually from the public food distribution system to distilleries. Going further raises serious food security exposure.

2G ethanol -made from agricultural residues like rice straw and bagasse -is the only feedstock pathway with the headroom to meet flex-fuel demand without enlarging food, water, or land-use conflicts.

The numbers underline why this matters: India generates roughly 160–180 million tonnes of paddy straw alone every year, a significant share of which is currently set on fire in Punjab and Haryana. Convert that residue stream into 2G ethanol, and India simultaneously addresses three problems with one supply chain -flex-fuel feedstock, stubble burning, and rural income.

The Hero–Maruti launches are the demand signal. The supply-side response is 2G ethanol -at scale, on a schedule that matches the OEM rollout.

Where Khaitan Bio Energy Fits In

The supply-side answer to the Hero–Maruti launches isn’t theoretical. It is being built, today, by companies like [Khaitan Bio Energy](https://khaitanbioenergy.com/), whose patented 2G ethanol technology is purpose-built for exactly this transition.

The company’s technology -developed by Mr Rohit Khaitan and validated through a BIRAC-supported pilot under the “Cellulosic Ethanol Pilot Plant for Rice Straw Management” project -establishes a commercially viable cellulose-to-sugars-to-ethanol pathway. Three credentials are directly relevant to the flex-fuel demand profile India is now building:

- The technology is certified at Technology Readiness Level 8 (TRL-8) by the Department of Biotechnology, Government of India -indicating commercial deployment readiness, not laboratory stage.

- It has been evaluated by the Centre for High Technology, Ministry of Petroleum and Natural Gas, and selected for setting up commercial biorefineries under the PM JI-VAN Yojana.

- It is one of the rare 2G platforms that fully valorises every component of lignocellulosic biomass -producing not only 2G ethanol but also high-purity precipitated silica and gypsum as co-products. This breakthrough in lignin valorisation transforms 2G unit economics from marginal to competitive, addressing the historic capital-intensity barrier.

Hero is putting flex-fuel motorcycles into the hands of millions of daily commuters. Maruti is putting an E100-capable car into the showroom of its most popular family hatchback. The fuel that runs those vehicles, increasingly, will have to come from the rice straw that currently

burns in Punjab and Haryana -converted into clean transport fuel through 2G technology platforms purpose-built for India’s flex-fuel decade.

The Road Ahead

Three OEM data points stitched together describe a market on the move:

- Hero MotoCorp has placed flex-fuel into its highest-volume two-wheeler segment, at a 4% price premium that mass-market consumers can absorb.

- Maruti Suzuki has placed an E100-capable car into its most popular family hatchback nameplate.

- Tata Motors is targeting a maiden FFV launch by early 2027; Toyota is piloting a flex-fuel strong hybrid Innova Hycross.

In aggregate, this is no longer a niche conversation. It is a structural transition unfolding inside the same week, across the same showroom floors, into the same volume segments that define Indian mobility.

The vehicles are arriving. The fuel network is being built (48 outlets today, 5,000 by end-2027). The price advantage is on the table (₹20 per litre below petrol).

What still has to scale, at the same pace, is the ethanol production capacity that can sustainably feed this demand -without taking food off Indian plates or water out of Indian aquifers. The Hero–Maruti week is the demand signal. 2G ethanol is the supply answer.

India’s flex-fuel future is no longer being debated in conference rooms. It is being launched in showrooms. The ethanol that runs it has to be built with the same urgency.

Frequently Asked Questions

Q1. Which flex-fuel vehicles did Hero MotoCorp and Maruti Suzuki launch in June 2026?

On June 3, 2026, Hero MotoCorp launched the Splendor+ Flex Fuel and HF Deluxe Flex Fuel -India’s first flex-fuel motorcycles in the 100cc commuter segment, capable of running on ethanol blends from E20 to E85. On June 4, 2026, Maruti Suzuki launched the Wagon R Flex Fuel (also called “Bioflex”) -India’s first flex-fuel passenger car, engineered for blends up to E100.

Q2. How much do the Hero and Maruti flex-fuel vehicles cost compared to their petrol versions?

Hero’s flex-fuel motorcycles are priced approximately 4% above their conventional petrol equivalents -a relatively small premium that makes them mass-market viable. The Maruti Wagon R Flex Fuel is priced at approximately ₹7.24 lakh ex-showroom, roughly ₹85,000 (about 12%) above a comparable petrol Wagon R. Industry executives have flagged the need for targeted GST reductions on FFVs to bring the car-side premium down.

Q3. Are these vehicles really cheaper to run than petrol vehicles?

Industry estimates suggest E85-driven flex-fuel vehicles could reduce per-kilometre fuel costs by 25–35%, but the actual savings depend on three factors: the durable price differential between ethanol and petrol (E85 is currently priced ₹20/litre below petrol at IndianOil outlets); ethanol’s lower energy density, which means more fuel volume to cover the same distance; and the geographic availability of E85 / E100 pumps. The most attractive economics will be in regions with stable ethanol supply and consistent pricing.

Q4. Will E85 and E100 fuel be available everywhere?

Not immediately. India launched E85 on June 5, 2026 at 48 public sector fuel stations. The Petroleum Ministry plans to expand E85 availability to 500 outlets by December 2026 and 5,000 outlets by December 2027. Coverage is expected to expand from ethanol-surplus regions (Maharashtra, Karnataka, UP, the National Capital Region) outward. E100-capable infrastructure will follow E85 rollout, likely in dedicated pumps modelled on Brazil’s hydrous-ethanol approach.

Q5. Which other automakers are launching flex-fuel vehicles in India?

Tata Motors Passenger Vehicles has indicated technology readiness and is targeting a maiden FFV launch by early 2027. Toyota Kirloskar is actively piloting a flex-fuel version of the Innova Hycross Strong Hybrid (homologation in progress). Suzuki Motorcycle India already sells the Gixxer SF 250 with E85 compatibility, and Honda offers the CB 300F on E85 -both in the premium two-wheeler segment. Hero MotoCorp CEO Harshavardhan Chitale has indicated multiple OEMs are ready to launch products as soon as the fuel network expands.

Q6. How does the flex-fuel push affect India’s ethanol demand outlook?

Substantially. According to InCred Research, total ethanol demand could rise from approximately 13 billion litres in FY 2026 to 29.63 billion litres by FY 2040 if flex-fuel vehicles reach 50% of new petrol-vehicle sales by FY 2036 -a 21% uplift above the E20-only base case. Meeting that demand sustainably is not possible with 1G ethanol (sugarcane, maize, rice) alone, because of water-use, food-security, and land-use ceilings. 2G ethanol from agricultural residues is the only feedstock pathway with the structural headroom to match the demand curve.

Q7. What is Khaitan Bio Energy’s role in India’s flex-fuel transition?

Khaitan Bio Energy holds patents for a 2G ethanol production technology certified at TRL-8 by the Department of Biotechnology and selected for commercial biorefinery development under the PM JI-VAN Yojana. The technology converts rice straw and other lignocellulosic biomass into ethanol, alongside high-value co-products like high-purity precipitated silica and gypsum -addressing the historic unit-economics challenge of 2G ethanol. For an India where Hero, Maruti, Tata and Toyota are now placing flex-fuel vehicles into the market, this kind of platform is the supply-side bridge that the demand curve will rely on.